How to Save Your First $100,000 in Record Time

Saving $100,000 is a significant financial milestone that requires dedication, smart planning, and disciplined execution. In today’s economic landscape, achieving this goal in record time demands a strategic approach that combines effective budgeting, wise investing, and avoiding common financial pitfalls. This guide will provide you with practical steps and insights to accelerate your journey towards your first $100,000 in savings.

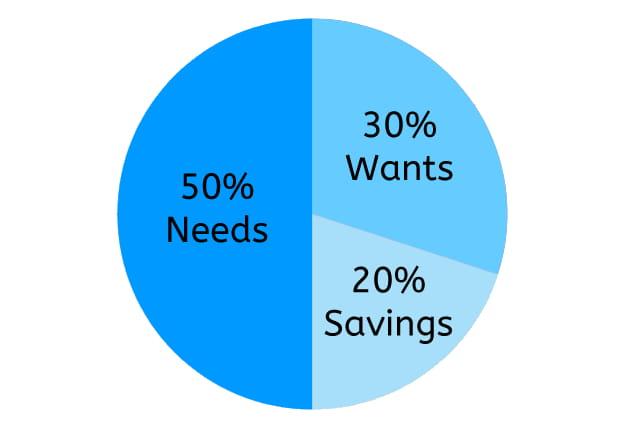

One of the fundamental steps in rapidly saving $100,000 is adopting a disciplined mindset and creating a budget that prioritizes savings. This involves carefully analyzing your income and expenses to identify areas where you can cut costs and redirect funds towards your savings goal. Implementing budgeting rules like the 50/30/20 or 70/20/10 can provide a structured framework for managing your finances, although these should be tailored to your specific circumstances.

To accelerate your savings, it’s crucial to reduce personal expenses by cutting nonessential costs. This might include limiting dining out, reducing entertainment expenses, or finding more cost-effective alternatives for your daily needs. Additionally, exploring ways to increase your income, such as taking on a side hustle or negotiating a raise at work, can significantly boost your saving potential. Overall, every dollar saved or earned is a step closer to your $100,000 goal.

Have you read?

- How to Invest for Beginners: A Comprehensive Guide

- How to Make Money Online for Free: 6 Legitimate Methods

- 30 Ways to Make Money Online: Quick and Easy Methods

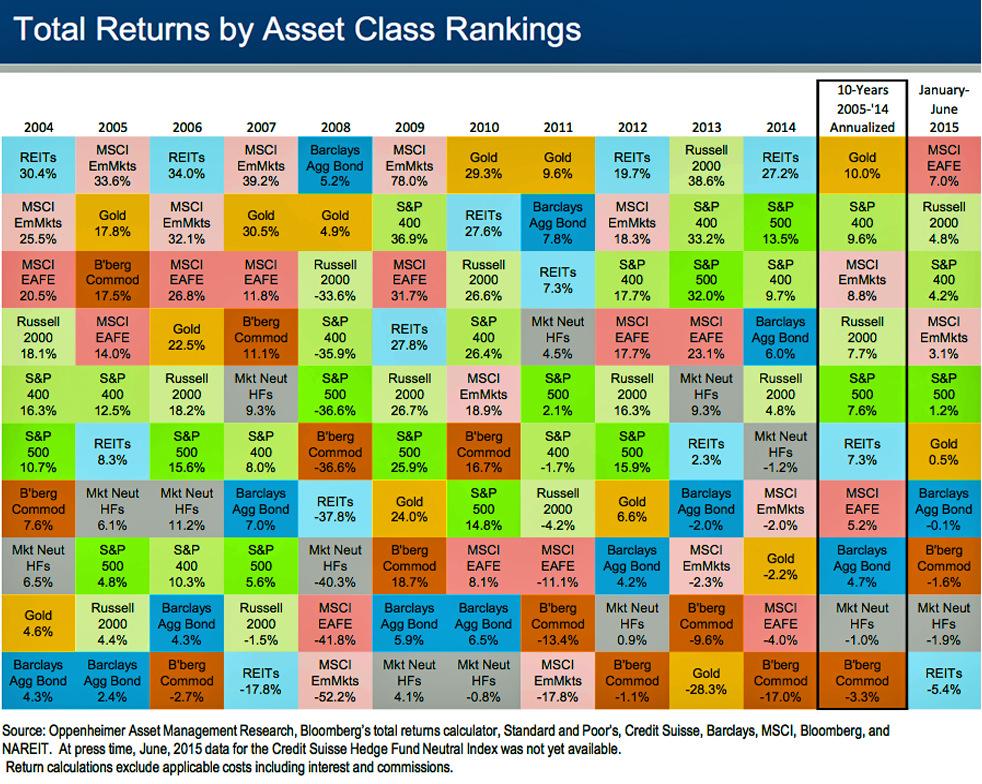

Investing plays a vital role in accelerating your journey to $100,000. By strategically allocating your savings into a diversified investment portfolio, you can potentially earn returns that outpace inflation and grow your wealth more rapidly. This approach allows you to balance risk and reward by spreading your investments across various asset classes such as stocks, bonds, and real estate. Over time, the power of compound interest can significantly amplify your savings.

When investing to reach your $100,000 goal, it’s important to consider the tax implications of your strategy. Holding investments for over a year can result in paying lower long-term capital gains taxes, which can enhance your overall savings. Additionally, having a clear plan for your investments is crucial to avoid losing value to inflation and to ensure you’re making intentional decisions aligned with your financial goals.

One common mistake to avoid when saving $100,000 is not having a diversified investment portfolio. Putting all your eggs in one basket can lead to missed opportunities for growth and increased risk. Instead, spread your investments across different asset types and regions to manage risk and potentially increase returns. This diversification strategy can help protect your savings from market volatility and provide more stable growth over time.

Another critical aspect of saving $100,000 quickly is utilizing budgeting tools and apps to track your expenses meticulously. These tools can help you identify areas where you’re overspending and provide insights into your financial habits. Having a clear picture of your spending patterns allows you to make informed decisions about where to cut costs and how to allocate your resources more effectively towards your savings goal.

Making lifestyle changes can significantly impact your ability to save $100,000 in record time. Consider cooking meals at home instead of eating out, using public transportation or carpooling to reduce transportation costs, and exploring options for downsizing your living arrangements. These changes may seem challenging at first, but they can lead to substantial savings over time and accelerate your progress towards your financial goal.

It’s essential to have both short-term and long-term plans for your savings as you work towards $100,000. For short-term savings, consider placing money in high-yield savings accounts to earn interest while maintaining liquidity. For long-term growth, explore investment options that align with your risk tolerance and time horizon. This balanced approach ensures that your money is working hard for you at all times, whether it’s needed in the near future or being saved for years to come.

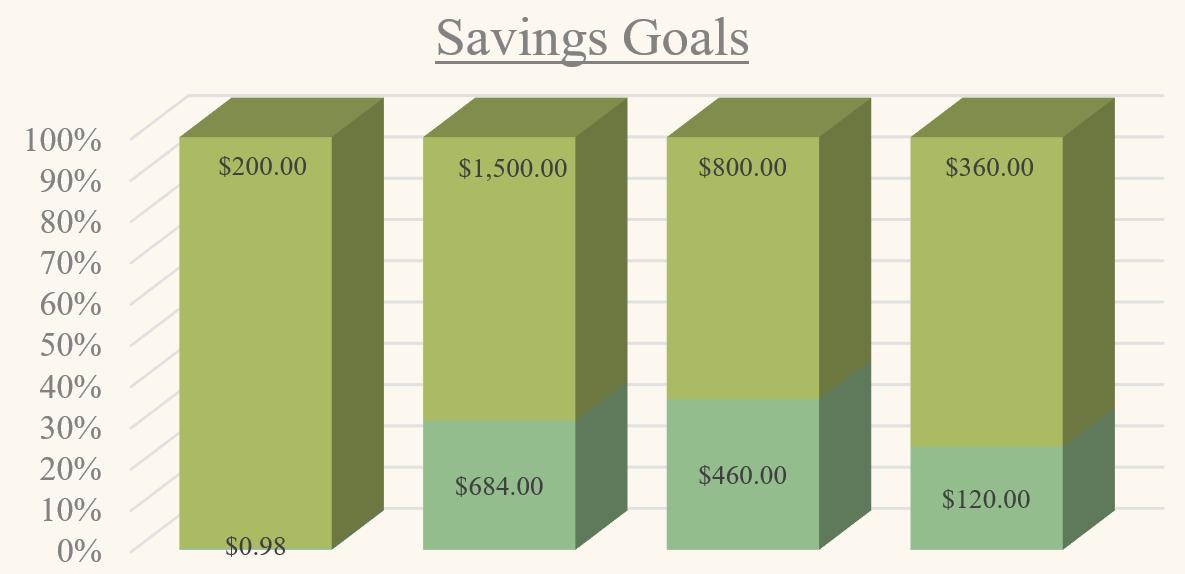

As you progress towards your $100,000 goal, it’s crucial to regularly evaluate your spending and set realistic financial milestones. This ongoing assessment allows you to adjust your strategy as needed and stay motivated throughout the process. Celebrate small victories along the way, such as reaching your first $10,000 or $50,000, to maintain momentum and reinforce your commitment to your ultimate goal.

While focusing on saving and investing, don’t overlook the importance of increasing your financial literacy. Stay informed about personal finance topics, tax strategies, and investment options. This knowledge will empower you to make better financial decisions and potentially uncover new opportunities to accelerate your savings. Consider reading financial books, attending workshops, or consulting with a financial advisor to enhance your understanding and refine your strategy.

Saving $100,000 isn’t just about cutting costs and investing wisely; it’s also about generating additional income streams. Explore opportunities for passive income, such as rental properties, dividend-paying stocks, or creating digital products. These additional revenue sources can significantly boost your savings rate and help you reach your goal faster. Be creative and leverage your skills and assets to generate extra income that can be directly channeled into your savings.

As you implement these strategies to save $100,000 in record time, maintain a long-term perspective and stay committed to your goal. There may be challenges and setbacks along the way, but with persistence and smart financial management, you can achieve this significant milestone.

Responses